For thousands of homeowners in Louisiana’s Terrebonne Parish, where 94% of homes were left without power after Hurricane Francine crossed its shore Thursday, any storm damage could have been catastrophic. One out of 4 of the 31,000 homeowners in the coastal parish live there without homeowners insurance — one of the highest percentages in the U.S.

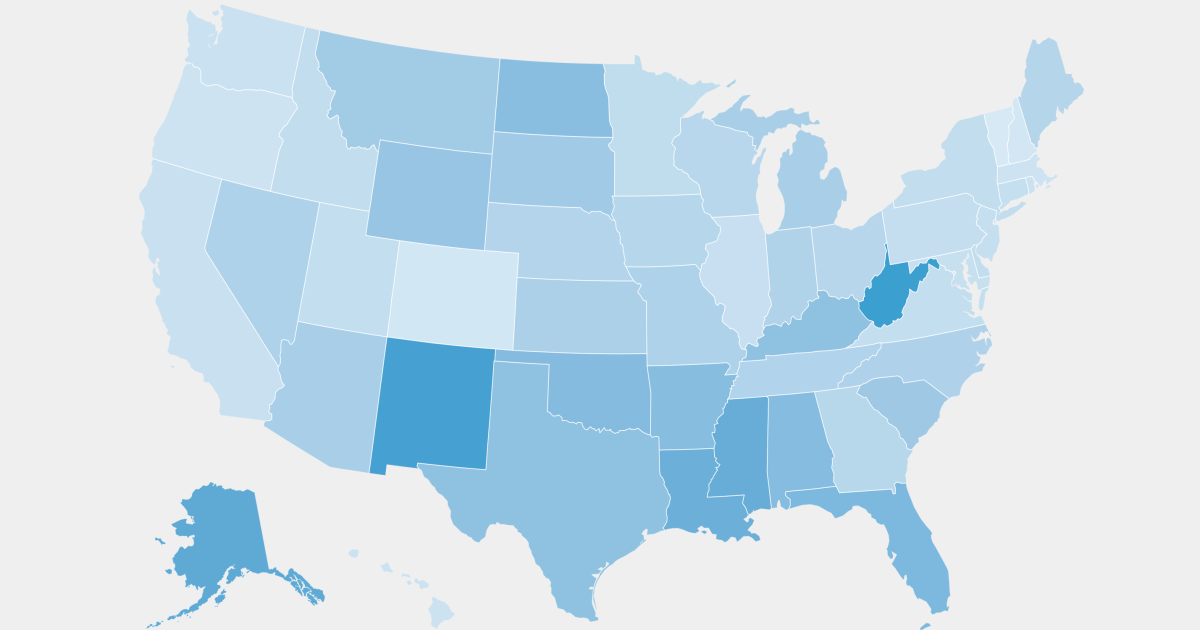

Across the country, 13.4% of homeowners — about 1 in 8 — are unprotected by homeowners insurance, according to an NBC News analysis of new Census Bureau data. Experts say that the number of households without meaningful insurance, which has rocketed in the past five years, is alarming and that it impedes recovery from natural disasters.

The share without insurance is highest in the South, where 15.7% of homeowners lack insurance entirely or pay so little for it that experts say the policies wouldn’t protect them. That’s a double bind in a region where households are both less financially able to weather severe climate events but — in many cases — more likely to experience them.

Under-insurance rates are higher in counties with majority-minority populations. Twenty-two percent of homeowners are uninsured in majority Native American and Native Alaskan counties, and 14% are uninsured in counties that are majority-Black.

“Not having insurance at all is just the worst-case scenario, especially if you still have a mortgage,” said Shannon Martin, an insurance analyst at Bankrate. “If you’re someone who can’t afford to pay your policy, you’re not someone who can afford to assume more risk. It’s a double-edged sword.”

The census data shows how many homeowners pay less than $100 — or nothing at all — for homeowners insurance. Martin said the range reflects households who either don’t have insurance or are so underinsured that it works out the same.

According to the Census Bureau survey, which was taken last year, 20.8% of homeowners without mortgages also lack meaningful homeowners insurance. Among mortgage-holders, 8.5% don’t have meaningful homeowners insurance — and while banks require owners with mortgages to have homeowners insurance, gaps in coverage do happen.

“If you’re looking at how do I feed my children, how do I pay for their clothes versus paying your insurance, it’s a no-brainer,” Martin said.

Compounding the issue is how much more expensive homeowners insurance policies have become. The rise in policy costs is driven by more catastrophic events and more people moving to high-risk locations, said Mark Friedlander, communications director for the Insurance Information Institute, a nonprofit research-focused trade organization.

And what happens when catastrophe strikes the uninsured?

“It is very hard, if not impossible, to recover from a catastrophic loss event, like from hurricanes, wildfires, tornadoes, the big three categories, without proper home insurance,” Friedlander said.

There’s also an impact beyond the walls of a home. “Insurance claim payments benefit not only those directly affected by loss,” Friedlander said in an email. “For example, many claim payments ultimately go to local auto repair shops, home improvement stores, contractors and health care facilities to fix cars, rebuild homes and provide medical treatment.”

On a broader scale, uneven recoveries can deepen existing divides. “There will be many difficult decisions to make about who gets bailed out and who doesn’t,” said Daryl Fairweather, Redfin’s chief economist. “And communities that tend to have more money, that are more valuable, are better able to lobby their politicians to help them.”

And it could intensify the housing cost crisis. “We have a shortage of homes,” Fairweather said. “As long as there’s a shortage, the homes that are spared [from natural disasters] will become even more valuable.”

Leave a Reply